AI Infrastructure Spending Surges as Big Tech Expands Capex

A massive capital expenditure cycle by the world’s largest technology infrastructure operators is fundamentally restructuring the global semiconductor supply chain. Meta Platforms, Alphabet, Microsoft, and Amazon are tracking toward a combined investment of up to $725 billion in 2026, directed primarily toward high-performance data centers, advanced networking hardware, and custom silicon clusters.

This unprecedented deployment of capital has shifted market power into the hands of the specialized memory manufacturers responsible for producing High Bandwidth Memory (HBM)—the critical hardware component packaged alongside modern artificial intelligence accelerators. In May 2026, this structural shift culminated in a historic market milestone: the world’s three dominant memory manufacturers—Samsung Electronics, SK Hynix, and Micron Technology—each crossed the $1 trillion market capitalization threshold simultaneously, driven by an industry-wide supply shortfall that has filled production orders through the end of the year.

Background

The current infrastructure constraint traces its origins back to the severe macroeconomic downturn of late 2022 and early 2023. Following a pandemic-era peak in personal computer and smartphone sales, consumer electronics demand collapsed, leading to the worst memory industry supply glut since the 2008 financial crisis. Operating profits at industry leader Samsung dropped by 95% in the first quarter of 2023, forcing the “Big Three” memory producers to cut conventional fabrication output by 15% to 25% and reduce overall capital expenditure budgets by nearly half.

However, the simultaneous public release of frontier large language models altered corporate demand parameters almost overnight. While chipmakers allowed conventional dynamic random-access memory (DRAM) and flash storage (NAND) inventories to draw down throughout 2023 to stabilize prices, the demand for high-performance server clusters exploded.

Advanced artificial intelligence servers require vastly greater quantities of system memory and significantly higher data-transfer speeds than traditional enterprise computing units. Because advanced packaging nodes require multiple years to build, scale, and validate, the production cuts implemented during the 2023 cyclical trough directly laid the groundwork for the acute physical supply constraints observed across the global market today.

Key Developments

The financial scale of the current buildout has completely eclipsed previous technological transition cycles. According to updated corporate guidance and market tracking data, the combined investment from the four primary hyper-scale cloud operators reached approximately $300 billion in 2025. Mid-year financial reviews indicate that this capital expenditure trajectory is accelerating sharply toward the $725 billion mark for the full year of 2026.

-

Amazon: Chief Executive Officer Andy Jassy confirmed the company’s aggressive investment strategy, maintaining an internal capital expenditure allocation of approximately $200 billion for the year. Jassy framed the infrastructure buildout as a generational operational priority, stating to shareholders that the firm intends to secure market leadership despite the near-term margin compression associated with such capital-intensive projects.

-

Microsoft and Alphabet: Both organizations have revised their 2026 expenditure forecasts upward, funneling cash into global data center expansions and proprietary internal silicon initiatives, such as Google’s Tensor Processing Unit (TPU) v5 infrastructure and Microsoft’s specialized Maia acceleration architectures.

-

Meta Platforms: Driven by the compute demands of training its open-source Llama model iterations, Meta escalated its capital spending forecast to a range of $60 billion to $65 billion, dedicated almost exclusively to building foundational compute clusters.

This sustained torrent of capital has caused an explosive revaluation of the memory layer. In May 2026, Samsung Electronics surpassed the $1 trillion valuation mark on May 6, followed by Micron Technology on May 26, and SK Hynix on May 27. The collective valuation of these three entities reached $4.1 trillion, a sixteenfold increase from their combined valuation of approximately $254 billion a decade prior.

Why It Matters

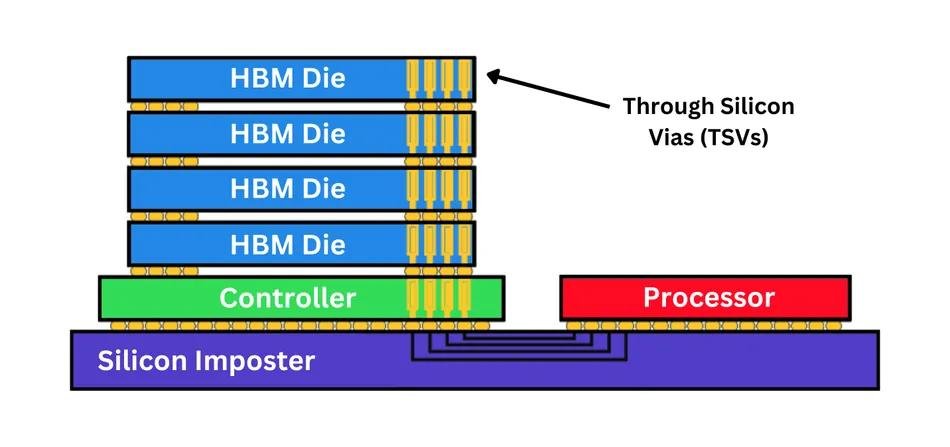

The defining physical limitation of modern high-performance computing is no longer raw processing velocity alone; it is memory bandwidth. Traditional memory designs present a data transfer bottleneck because data must travel across a motherboard from separate memory modules to the main processor. High Bandwidth Memory resolves this latency penalty by re-engineering the physical architecture of the chip stack.

As illustrated in the structural cross-section above, HBM bypasses traditional physical space constraints by stacking up to 12—and increasingly 16—individual DRAM dies vertically on top of a centralized controller. These stacked layers are interconnected using thousands of microscopic vertical channels called Through Silicon Vias (TSVs).

The entire memory stack is then placed directly next to the primary processor chip on a shared platform known as a silicon interposer. This physical proximity dramatically shortens the distance signals must travel, allowing the hardware to achieve memory bus widths exceeding 1,024 bits—far surpassing the 32-bit or 64-bit paths found in standard enterprise memory architectures.

Without this specialized architectural pairing, high-performance processors sit idle waiting for data packets to arrive, a phenomenon known in server design as the “memory wall.” Because every modern AI cluster deployed by hyperscalers depends entirely on this tight hardware coupling, control of HBM manufacturing has become the primary point of leverage in the global tech ecosystem.

Industry Perspective

The sheer velocity of this capital expenditure cycle has divided Wall Street and the broader technology sector into two distinct analytical camps regarding long-term market sustainability.

Inside the technology firms, executives argue that current spending patterns are entirely rational responses to hard demand backlogs. For instance, Alphabet reported that its cloud revenue grew by more than 60%, with its future customer backlog nearly doubling over a single quarter to $460 billion. Similarly, Microsoft noted that its specialized enterprise AI segment has reached an annualized revenue run rate of $37 billion, reflecting a 123% year-over-year expansion. From the hyperscaler perspective, underspending presents a far greater existential threat to market share than overspending.

Conversely, institutional skeptics warn of an asset pricing bubble reminiscent of the telecommunications overbuild of the late 1990s.

“You are seeing orders and sales booked today, while the physical costs to the buyer are spread over amortization periods extending up to ten years,” explained Justin Kersmanc, portfolio manager at GQG Partners, which has rotated its flagship funds away from infrastructure stocks. “The core issue is not whether demand is strong today, but whether that demand is economically justified and sustainable once return on investment, utilization, and corporate pricing power are fully tested in the real economy.”

Furthermore, macroeconomic researchers at Goldman Sachs estimate that total ecosystem capital expenditures could scale to $7.6 trillion globally through 2031 to build out the required data center footprint. Analysts express growing concern that while foundational infrastructure companies are booking immediate profits, actual end-user revenue from retail and enterprise software products remains highly concentrated and insufficiently large to support the underlying hardware costs over a multi-year horizon.

Market or Consumer Impact

The prioritization of high-bandwidth infrastructure is producing significant downstream distortions across the broader commercial electronics sector. Because HBM manufacturing consumes significantly more physical silicon wafer capacity than standard DRAM—often requiring up to three times the wafer area to produce an equivalent number of bits due to the complexity of vertical stacking and lower production yields—the entire global chip supply has contracted.

This manufacturing shift has caused widespread supply shortages across conventional enterprise memory, lower-power mobile phone components (LPDDR5), and high-capacity solid-state storage drives (NAND SSDs). With fabrication lines running at absolute capacity, memory manufacturers hold historic pricing power. Enterprise contract prices for storage and memory components are projected to climb by 134% over the course of 2026.

For corporate buyers and enterprise data center operators outside of the core hyperscale group, the cost of sourcing standard server components has surged, extending hardware replacement cycles and driving up cloud container leasing costs. For everyday consumers, these supply line diversions are expected to materialize as increased retail pricing for high-end personal computers, gaming consoles, and flagship smartphones heading into the winter product cycles.

Future Outlook & Conclusion

The competitive landscape among memory producers is set to intensify in the second half of 2026 as the industry transitions from current HBM3E hardware to the next-generation HBM4 standard. This structural shift will represent a major engineering change: for the first time, the foundational controller die at the bottom of the memory stack will be manufactured using advanced foundry processes rather than standard memory fabrication lines.

| Manufacturer | Q1 2026 HBM Market Share | Strategic Focus & Technical Roadmaps |

| SK Hynix | 58% | Maintaining market leadership via multi-year supply exclusivity deals; shifting to advanced packaging nodes. |

| Samsung Electronics | 21% | Accelerating HBM4 production; leveraging its internal advanced foundry to manufacture custom base dies. |

| Micron Technology | 21% | Capitalizing on U.S. domestic fabrication facilities, emphasizing lower power-consumption metrics. |

While SK Hynix maintained a dominant 58% share of the HBM market in the first quarter of 2026, Samsung is positioned to weaponize its internal semiconductor foundry divisions to produce these integrated custom base pieces natively, aiming to recapture market share as shipments materialize in late 2026. Simultaneously, Micron is leveraging its position as the primary onshore U.S. manufacturer, riding a wave of domestic supply-chain security mandates from Washington to offset the massive scale of its South Korean peers.

Ultimately, the global technology sector finds itself fully committed to a structural transition that cannot easily be reversed. Even if consumer software demand experiences a temporary plateau, the multi-year manufacturing facilities currently being built in East Asia and the United States will proceed to completion. The global computing stack is being physically reconstructed from the silicon layer up, lock-stepping the future of international finance with the raw production capacity of exactly three memory manufacturers.

Frequently Asked Questions

1. What is driving the sudden surge in Big Tech capital expenditures in 2026?

The increase is driven by the scaling requirements of frontier artificial intelligence models, which require massive computing power for training, alongside a sharp rise in inference demand as enterprise products are deployed across commercial cloud networks.

2. Why are memory companies crossing the $1 trillion market cap threshold now?

High Bandwidth Memory (HBM) has become the primary physical bottleneck for high-performance computing. Because only three companies can manufacture this hardware at scale, they possess immense pricing power, translating into historic revenues and unprecedented market valuations.

3. What exactly is High Bandwidth Memory (HBM)?

HBM is a specialized form of dynamic random-access memory (DRAM) where individual memory chips are stacked vertically and linked via microscopic vertical wires. This stack sits directly next to the main processor on a shared platform, drastically increasing data transfer speeds.

4. How does HBM differ from the standard RAM used in consumer PCs?

Standard RAM modules are placed further away from the processor on a motherboard, communicating across narrow, slower data paths. HBM uses vertical stacking and a wider interface directly adjacent to the processor, clearing the latency bottlenecks that slow down complex workloads.

5. Which company currently leads the High Bandwidth Memory market?

SK Hynix maintains market leadership, holding a 58% share of the global HBM market in the first quarter of 2026, though Samsung and Micron are expanding production rapidly to capture market share.

6. Is there a risk of a structural oversupply or an AI infrastructure bubble?

Yes. Institutional asset managers have warned that capital expenditures are scaling far ahead of proven end-user software revenues. If commercial monetization slows down, the industry could face a severe overcapacity problem.

7. Why can’t memory makers simply build more factories to fix the shortage?

Building modern semiconductor fabrication facilities requires multiple billions of dollars and typically takes two to three years for construction, cleanroom installation, and manufacturing validation before commercial production can scale.

8. How does the HBM shortage impact everyday consumer electronics?

Because HBM manufacturing consumes up to three times the physical silicon wafer area of standard memory, production lines have shifted away from consumer chips. This has triggered price increases and supply constraints for smartphones, laptops, and gaming systems.

9. What major technical transition is expected in the second half of 2026?

The semiconductor industry is transitioning to the HBM4 standard, which will integrate logic foundry processes into the base of the memory stack, allowing for deeper customization and direct processing adjustments.

10. How do U.S. domestic manufacturing policies fit into this ecosystem?

Micron Technology, as the sole major U.S.-based memory manufacturer, is expanding its domestic capacity to benefit from government supply-chain localization mandates, providing geographic diversification away from East Asian supply lines.